Prior to this case, $fuboTV Inc.(FUBO)$ had been fighting an "antitrust lawsuit" from Venu Sports.Venu Sports is a sports streaming service launched by $Walt Disney(DIS)$ $Warner Bros. Discovery(WBD)$ and $Fox Corporation Class B(FOX)$ a joint sports streaming service.

Fubo believes that Venu is deliberately motivated to prevent distributors like Fubo from accessing unbundled sports content, and therefore can would likely substantially lessen competition in the marketplace, and therefore progress through the end of 2024 has been made to gain the support of the DOJ, and also the support of a number of states, including NY, CA, IL, and others.

The short answer is that Fubo is suing Venu and Venu is currently at a disadvantage.

So for DIS, can't settle the legal dispute, so they settle the other side.

Fubo is just a small company, after all.

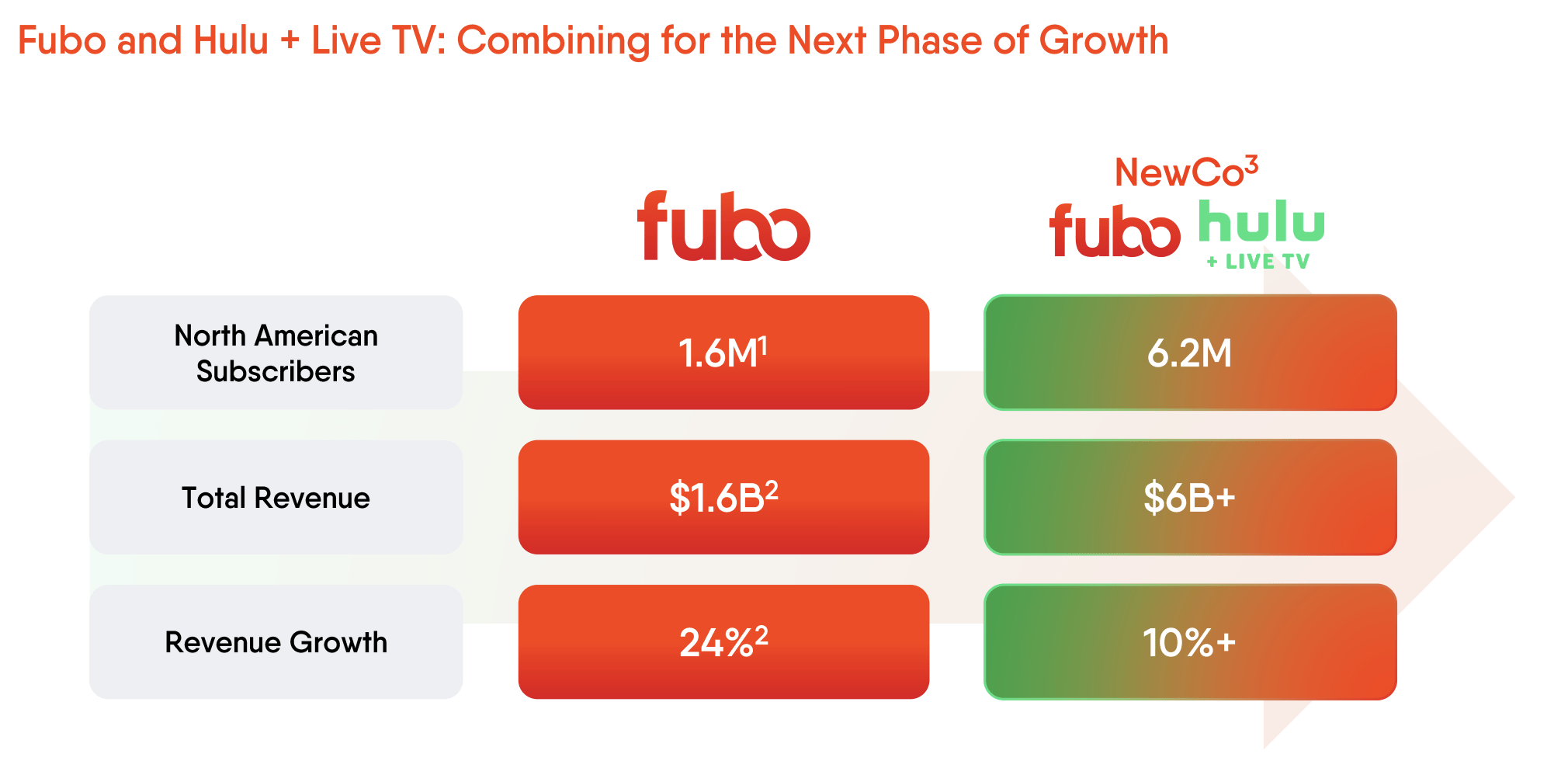

FUBO and DIS said Monday that they will merge their Hulu + Live TV business with Fubo to create a new venture, in which DIS holds a 70 percent controlling stake, that will serve more than 6.2 million customers in North America.

FUBO's stock rose more than 200 percent in pre-market trading on the New York Stock Exchange.

The agreement includes:

Fubo's existing management team will run the new business, with the CEO remaining Fubo's David Gandler (whether or not he'll cross the river in the future is unknown; Disney itself changes hands pretty frequently), while the new entity is expected to be "well-capitalized and cash-flow positive" after the deal closes.

As part of the deal, Fubo agreed to settle all litigation with Disney regarding Venu Sports, and to settle all litigation with FOX and Wah WBD

DIS, FOX, and WBD will pay Fubo $220 million in litigation fees

DIS has committed to a $145 million term loan in 2026 to the new company, Fubo.

Fubo will create a new sports and broadcast service that will include Disney's sports and broadcast networks (ABC, ESPN, ESPN2, ESPNU, SECN, ACCN, ESPNEWS and ESPN+).

Both Fubo and Hulu+Live TV will continue to be available to consumers as separate products after the deal closes;

Under certain circumstances, DIS pays Fubo a termination fee of $130 million if the deal fails.

A couple of caveats to the deal

Fubo is perennially losing money and can't afford to drag out prolonged litigation, so being acquired may be the best possible outcome; for DIS, that leaves the cost of litigation, as well as saving Venu Sports' operating costs.

The cost of the live sports industry is rising every year, and the merged company is expected to gain more pricing power, but still needs regulatory approval;

Considering the current YouTube TV $Alphabet(GOOG)$ and $Netflix(NFLX)$ are promoting the live streaming sports business, it is expected that the antitrust pressure is not big, and the deal is more certain;

In the long run, the potential of the sports market is still large, but the competition will also be fierce.From a streaming perspective, Netflix and YouTube TV are growing more than Fubo, and even with Disney's ESPN+ and Hulu+Live, a three-way split is likely in the future;

In the short term, the biggest question mark is the valuation of Fubo, and the focus is on the average value of the customers that the two companies state they "serve more than 6.2 million customers in North America".

How much is the new Fubo worth?

Take Q3 2024 numbers:

FUBO has 1.99 million subscribers with an ARPU of $93.14; 1.61 million of those are in North America, with a North American ARPU of $85.64.

DIS's HULU + LiveTV + SVOD supply 4.6 million subscribers with an ARPU of $95.82, basically all in North America.

Using DIS's 4.6 million households in 24Q3, which contributed $440 million in revenue, if DIS's market capitalization is calculated as a multiple of revenue and the different businesses bring in the same revenue (actually valuing the streaming portion of the business a bit lower than the offline parks), the North American portion of this brings in 2% of the revenue.

If all 6.2 million of Fubo's new company's households are active customers and ARPU can be maintained at $95.82, FUBO could be valued at $5.29 billion using the DIS valuation.

FUBO's market capitalization was $1.7 billion at the close of trading on January 6, which translates into a market capitalization of around $5.5-5.6 billion, taking into account the percentage of additional shares issued at the time of the merger.

Therefore, the current price of FUBO has basically reflected the valuation of DIS's Hulu Live+, and does not take into account the "Dyssynergy" factor.

However, if investors are trading FUBO on the basis of meme shares, the valuation may not really matter, and sentiment may be stronger in the short term, but for Disney investors, they may need to consider the results of spinning off parts of the business.

Comments