Solid Quality, Even if the Headline Wasn’t Spectacular

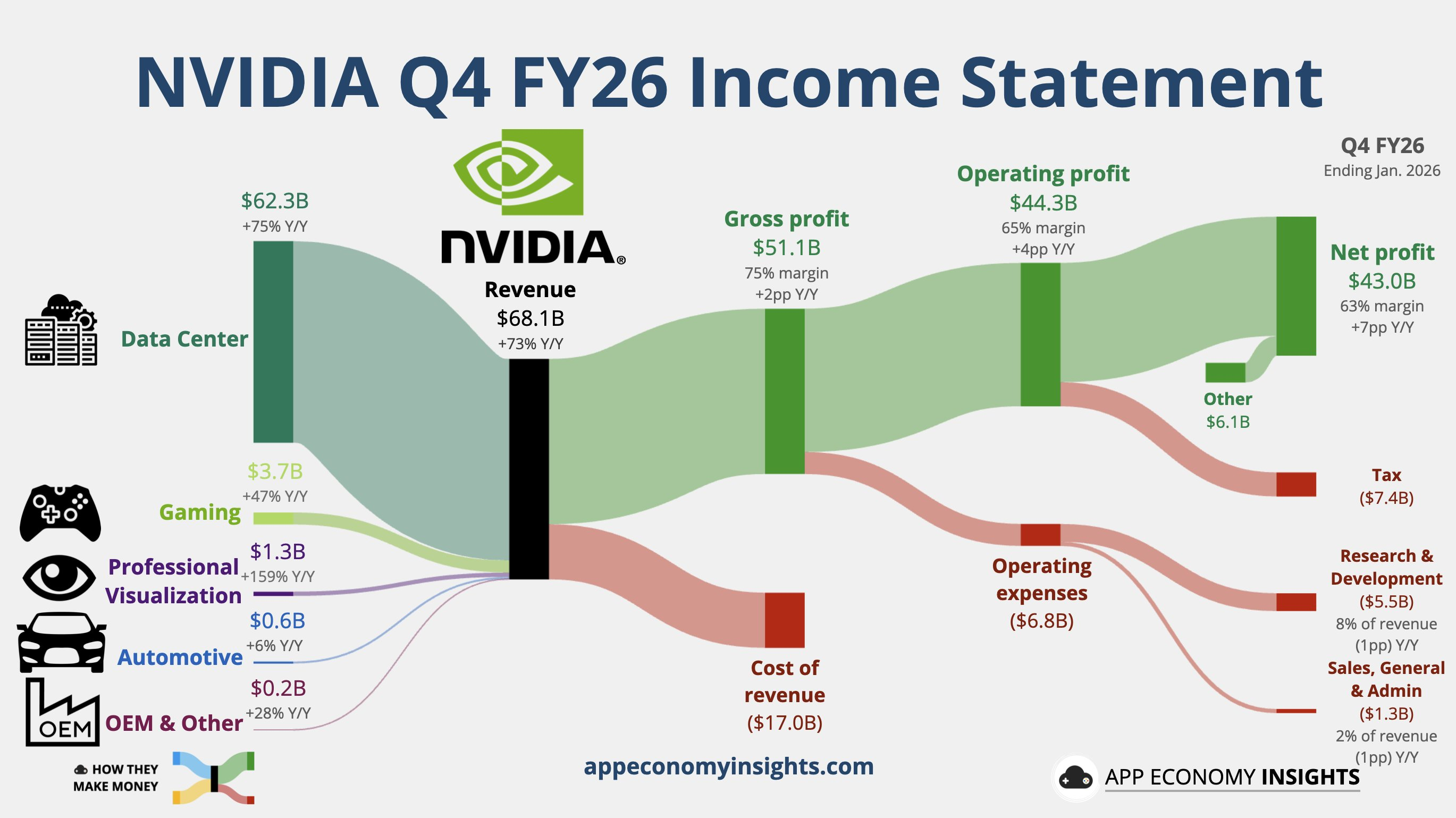

$NVIDIA(NVDA)$ reported FY26 Q4 revenue of $68.1 billion, modestly ahead of consensus, with adjusted EPS of $1.62, also slightly above expectations. Revenue grew 73% year over year and 19.5% sequentially. Sustaining this growth rate at a $4.8 trillion market capitalization is, in itself, exceptional.

Data Center revenue reached $62.3 billion, accounting for 91% of total revenue and remaining the core growth engine. Within the segment, Compute (GPU and Grace CPU) came in slightly below expectations, while Networking significantly outperformed, exceeding estimates by roughly 13–27% and showing stronger sequential and year-over-year growth. This suggests AI infrastructure buildout is progressing beyond incremental compute purchases toward full-stack system deployment. AI data center expansion is becoming increasingly systematic and scaled.

Gaming revenue was $3.7 billion, below expectations, with management attributing the shortfall to supply constraints. Capacity continues to be strategically prioritized toward Data Center, reflecting allocation discipline rather than end-demand deterioration.

Professional Visualization revenue of $1.3 billion materially exceeded expectations. While relatively small in size, this segment often serves as a leading indicator of enterprise AI adoption.

Overall, quarterly revenue and earnings were not explosive, but the composition remains healthy and growth drivers are clearly concentrated in AI infrastructure.

Gross Margin at 75% Reinforces Pricing Power

Adjusted Q4 gross margin was 75.2%, above expectations. Despite continued increases in HBM pricing, management guided for gross margins to remain in the mid-70% range for the full year, underscoring strong cost control and pricing power.

Operating margin reached 67.7%, and rapid Data Center expansion has not materially diluted profitability. Advanced packaging and memory cost pressures have been effectively offset. This reflects both proactive memory procurement strategies and the premium positioning of high-end AI products.

In the current semiconductor landscape, maintaining ~75% gross margin during a period of hyper-growth is rare. AI compute supply remains structurally tight, supporting NVIDIA’s pricing leverage.

Balance Sheet: Disciplined Expansion, Not Channel Stuffing

Investors have closely monitored accounts receivable and inventory.

Accounts receivable totaled $38.5 billion, up 67% year over year—below the 73% revenue growth rate and slower than the prior quarter. Days Sales Outstanding rose modestly to 51 days but remains manageable. The divergence between revenue growth and receivables growth indicates disciplined credit management. The company is not extending aggressive payment terms to sustain top-line growth.

This also suggests that downstream customer cash flows have not meaningfully improved; AI monetization cycles are still maturing. Management appears cautious in risk control.

Inventory reached $21.4 billion, up 112% year over year but decelerating from the prior quarter’s 158% growth. Finished goods now account for 41% of inventory, up meaningfully. Viewed in isolation, this could raise demand concerns. However, guidance provides critical context.

Guidance Significantly Ahead of Expectations

Management guided next-quarter revenue to a midpoint of $78 billion, more than 8% above consensus (~$72.1 billion). Gross margin guidance remains at 75%.

This level of guidance is notably strong and provides a clearer explanation for the inventory mix shift. The increase in finished goods is more likely preparation for elevated shipment volumes rather than evidence of demand softening. If demand were weakening, such an aggressive revenue outlook would be unlikely.

This implies that cloud hyperscaler procurement in calendar 1Q26 will accelerate further. AI capital expenditure momentum remains intact in the near term.

Earnings Call: Limited Incremental Detail, Focus Shifts to 2027

The earnings call offered limited new disclosures. Management was measured in addressing longer-term questions.

A key analyst question centered on whether growth could be sustained if large technology customers are unable to further increase capital expenditures in 2027. Management emphasized that compute drives customer revenue generation and maintained confidence in demand durability, but did not provide a detailed framework for post-2026 growth. This leaves open concerns around growth normalization in 2027.

Management also reiterated that it does not plan to develop custom chips internally, emphasizing efficiency in concentrating resources on its core architecture.

The company indicated that its investment and partnership with OpenAI is nearing completion and confirmed its investment in Anthropic. Collaboration with Meta Platforms has also deepened. These capital and ecosystem linkages reinforce long-term platform stickiness, though near-term financial impact is limited.

Markets may look to the upcoming GTC conference for greater clarity on next-generation products and architectural roadmaps.

Valuation: Entering the Execution Phase

At approximately $195 per share, the stock trades at roughly:

-

~16x 2027 earnings

-

~13x 2028 earnings

If earnings projections materialize, valuation appears reasonable. However, investor focus has shifted from demand acceleration to durability of growth.

Near-term earnings visibility remains high and risk appears manageable. Medium-term performance will depend on:

-

2027 capital expenditure trends

-

Rubin platform ramp timing

-

AI commercialization progress

Share price action may remain range-bound in the first half of the year. Clearer visibility into Rubin production and 2027 order trajectories in the second half could be required for multiple expansion.

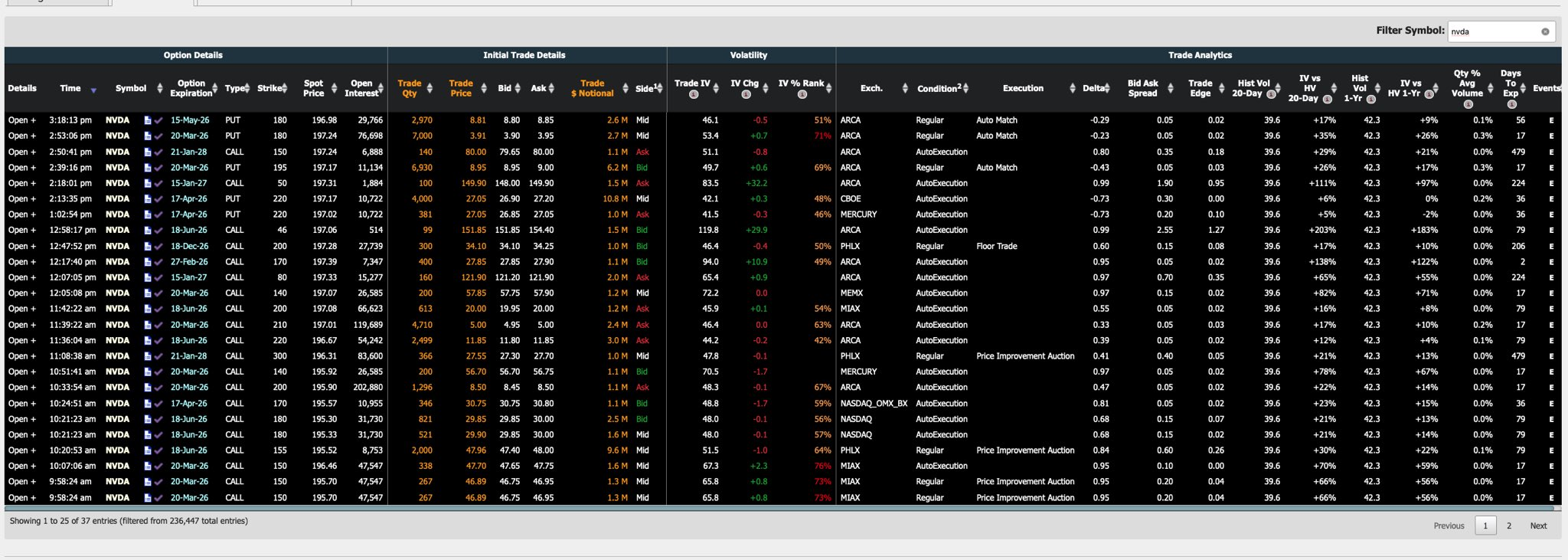

Options Flow Around Earnings

Options activity around NVDA shows multiple large block trades concentrated in March and June expirations, alongside structured positioning in longer-dated 2027–2028 contracts. The overall pattern suggests short- and medium-term directional positioning, supplemented by long-dated high-delta leverage structures.

In near-term flows, repeated trades in the March 20 $150 calls (267 and 338 contracts, among others) were executed at $46–47 with delta around 0.95 and implied volatility in the 73–76% range. These deep in-the-money calls function as leveraged stock substitutes. Individual notional sizes of approximately $1.3 million and repeated executions suggest institutional directional accumulation following earnings. With delta near 1, these positions are highly sensitive to further upside.

Also notable were 1,296 contracts of March $200 calls, with notional exposure near $11 million and delta around 0.47. This represents a classic near-term upside expression. Despite elevated post-earnings implied volatility (~48%), buyers were willing to pay time premium, implying confidence in a potential break above the $200 level in the coming month.

June $180 calls (821 and 521 contracts) traded around $30 with delta ~0.68, representing medium-term bullish positioning for the first half of the year rather than purely event-driven trades.

Long-dated positioning is particularly notable. January 2028 $150 calls (140 contracts at $80, delta ~0.80) reflect longer-term conviction. Implied volatility around 51% suggests rational long-term volatility pricing. Such structures often serve as stock replacement positions.

On the defensive side, 6,930 contracts of March 2026 $195 puts traded (notional ~$6.2 million, delta ~-0.43). Given concurrent call activity, this likely represents protective hedging rather than outright bearish positioning.

More extreme leverage was visible in January 2027 $50 deep in-the-money calls (delta near 1, IV ~83%), typically associated with capital efficiency optimization or LEAP-style stock replacement.

Options Market Takeaways

Three patterns stand out:

-

Active near-term call buying in the $150–$200 range, indicating continued short-term upside expectations.

-

Increased medium-term positioning into June expirations, reflecting confidence in first-half momentum.

-

Ongoing accumulation of long-dated high-delta calls, signaling sustained long-term conviction.

Implied volatility generally ranges between 46% and 70%, with IV Rank mostly between 50% and 70%, suggesting neither extreme complacency nor panic. Current flows appear driven by directional positioning rather than volatility arbitrage.

Overall, the options market reflects structural bullish positioning at elevated levels, complemented by selective protective hedging. There is little evidence of systemic de-risking. Near-term focus remains on a potential break above $200, while medium-term direction will likely hinge on GTC disclosures and order visibility.

Comments