$Tesla Inc.(TSLA)$ is set to report quarterly results after the U.S. market close on April 22. Options positioning into the print points to a cautious tone. Block trades suggest investors are buying deep out-of-the-money (OTM) puts as “insurance” against a sharp near-term drawdown, while simultaneously selling longer-dated deep OTM calls, signaling skepticism about the scope for a strong medium-term rally. The options market implies a post-earnings trading range of roughly $365.7 to $419.3.

1) Earnings expectations and key watch points

Consensus estimates (this quarter):

-

Revenue: $22.713 billion, +7.58% YoY

-

EPS: $0.373, -4.73% YoY

-

EBIT: $959 million, -8.01% YoY

Focus areas: Investors will be watching auto gross margins (amid pricing pressure and costs), growth in the energy storage segment, progress in software revenues such as FSD, and capital spending tied to AI and robotics.

2) Options metrics: implied volatility and open interest

(1) Implied move

Based on options expiring Friday (April 24), implied volatility stands at 75.32%, pointing to an expected post-earnings move of about ±6.83%.

-

Reference price: ~$392.50

-

Implied range: $365.70 – $419.30

Elevated IV reflects broad expectations for a sizable earnings-driven swing.

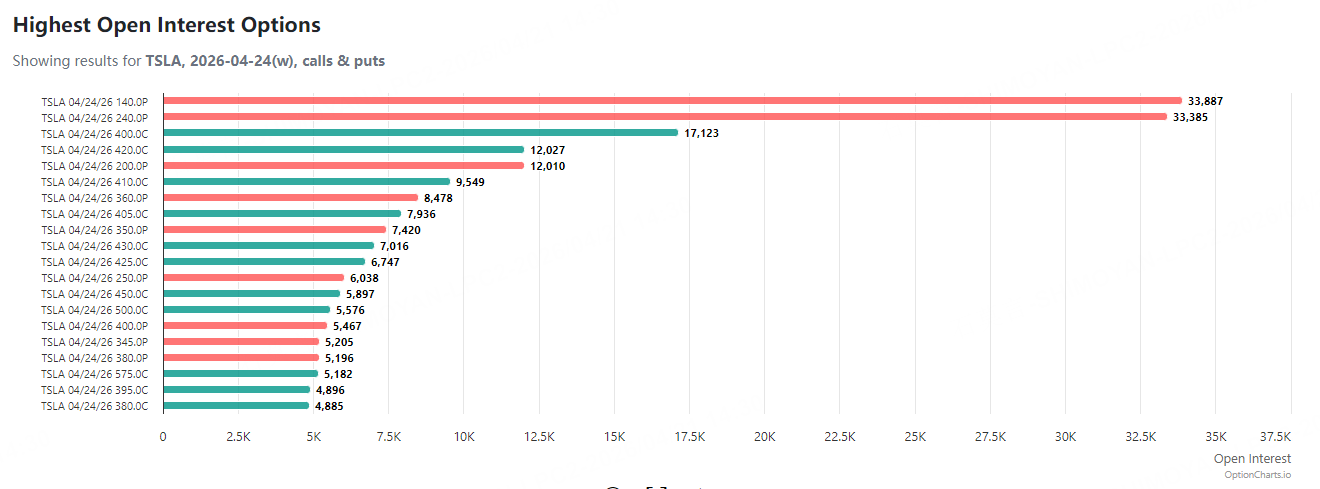

(2) Open interest distribution

As of April 21, positioning in April 24 expiries shows clear clustering:

-

Puts: OI concentrated at $350 (7,420 contracts) and $360 (8,478 contracts)

-

Calls: $400 (17,123 contracts) is the largest call strike, followed by $420 (12,010 contracts)

3) Block activity: reading institutional intent

Large trades over the past three sessions outline a cautious playbook: hedge near-term downside, avoid chasing upside.

(1) Largest single trade: buying short-dated “disaster insurance”

-

Contract: TSLA Apr 24, 2026 $310 Put

-

Action: Bought 6,371 contracts

Rationale: A highly convex bet. Traders paid a small premium (~$0.16 per contract) for deep OTM puts expiring this week, implying either a hedge against a tail-risk “black swan” drop or a low-cost lottery on an extreme post-earnings selloff.

(2) Largest premium strategy: selling medium-term “lottery tickets”

-

Contract: TSLA Jul 17, 2026 $500 Call

-

Action: Sold 2,099 contracts (across two blocks)

-

Notional premium: ~$1.63 million

Rationale: A classic theta (income) strategy. Sellers view a move from ~$390 to $500 within three months as unlikely, and monetize time decay by collecting relatively rich premiums (~$7.6–$7.9 per contract). This underscores institutional skepticism toward a sharp medium-term rally.

(3) Other notable flow

-

Short puts: Sale of 2,000 contracts of May 1, 2026 $345 Put

-

Likely a cash-secured put strategy, indicating willingness to accumulate shares around $345.

Sentiment takeaway: Block flows indicate downside protection into earnings, paired with conservative medium-term upside expectations. The bias is toward premium collection strategies rather than directional bets.

4) Strategy considerations

For option sellers:

Extreme strikes (e.g., $500 calls, $310 puts) are priced with elevated premiums. For those expecting a less dramatic move, deep OTM options offer attractive income opportunities. Selling far OTM calls—akin to the $500 strike—appears to carry a relatively high probability of success, assuming volatility subsides post-event.

For option buyers and risk control:

Buying near-dated deep OTM options (such as the $310 put) is a high-risk, high-leverage trade akin to purchasing a lottery ticket. Investors seeking defined risk may consider spread structures (e.g., put spreads) instead of outright long puts, to reduce cost and cap downside exposure.

Comments