Summary

- Contrary to popular belief, Microsoft is still a growth name.

- Microsoft's bottom line EPS continues to demonstrate high growth, with Q4 2021 growing by 42% y/y (currency-adjusted).

- By my estimates, the stock trades for approx. 28x forward EPS.

- Not too many companies out there in tech have EPS numbers. And those that do, are not being priced below their CAGR. Microsoft is an exception.

Investment Thesis

Microsoft (MSFT) put out very strong growth in Q4 2021, with its top-line growing by 21% y/y. Thus, this result fully justifies its stock's performance in the past twelve months.

What's more, looking ahead, by my estimates, its EPS could grow to $10.36 leaving the stock trading at 28x forward sales.

Microsoft remains a worthy investment consideration, even now.

Investor Sentiment Facing Microsoft

This is the first quarter that we are now fully lapping the pandemic's comparables.

And even though by this stage investors should be coming to terms and adjusting themselves into what's a permanent change and the new normal and what's a should be compared to pre-COVID periods, I feel we are none the wiser.

To this end, the fact that this tech behemoth put up such a strong result yet the after-hours reaction was so muted, as were both Apple (AAPL) and Alphabet (GOOGL)(GOOG), presents investors with a conundrum: is it all possible that investors expected aneven bigger positive surprise from these names?

Moreover, keep in mind that behind the big push by the mega-caps that are now trading at close to all-time highs, many smaller caps stocks are well into correction territory in 2021. Correction territory means trading 20% or more from previous highs. Indeed, this discrepancy between large caps and small caps is truly fascinating.

To this end, I can only conclude that in the short term the market is a voting machine and that in time, Microsoft's bottom line profitability will continue to drive its stock forward. So let's dig in further to Microsoft's results.

Revenue Growth Rates Are Still Strong

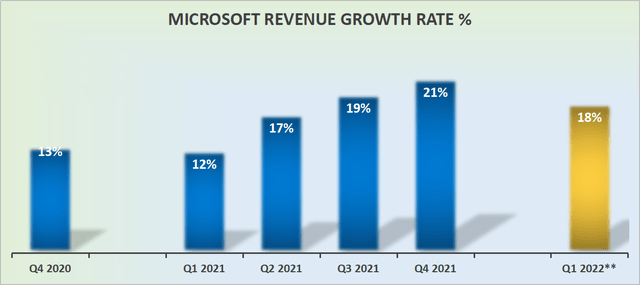

As you can see above, Microsoft's growth rates during fiscal 2021 actually accelerated. During Q4 2021, Microsoft's top line increased by 21% y/y.Is there a time when the law of large numbers starts to slow down this giant?

Common sense answers in the affirmative. But the factual results show that bringing in more than $46 billion in revenues during a 90 day period is an achievable feat for Microsoft.

Looking out at its guide ahead, we can see that Microsoft's momentum continues to be very strong. If investors had reasons to expect a strong performance this quarter as Microsoft had slightly easier comps, the high-end guidance for next quarter fully dispels the myth that Microsoft is anything but a high growth name.

In 2021 Microsoft is more diversified than it's ever been: With Search advertising Bing up 53% y/y, to LinkedIn being up 46% y/y, as well as Microsoft's ERP (Enterprise Resource Planning) Dynamics 365 up 49%, but real needle mover is obviously Microsoft's commercial cloud.

The Crown Jewel in the Quarter: Commercial Cloud

Microsoft's commercial cloud was up 36% y/y to $19.5 billion. Within that, Azure was up 45% (at constant currency).

Microsoft's ability to engage both old and new enterprises, while at the same time offering a differentiated enough cloud platform so customers' usage and demand remains high, speaks to the power of Microsoft's brand.

So when I questioned whether or not Microsoft has what it takes to break free from the law of large numbers, I believe we should invert the question. The question needs to be is there a physical reasonwhy Microsoft can't put up strong numbersfor another decade?

I don't believe there is. On the one hand, smaller enterprises are being sold on the idea that this household name is the no-brainer cloud platform to adopt. But at the same time, Microsoft's multi-year investment to invest in cloud engineering is being reflected in its numbers.

For example,75% of the Fortune 500 use Microsoft's hybrid offerings. These are companies with the financial resources and technical acumen to demand only the best of the best hybrid cloud. And by far and wide, the bulk of these global enterprises still chose Microsoft's cloud platform.

Also, and this important, unlike countless other fast-growing names in tech right now, that have no clear path to profitability, Microsoft has incredibly high profit margins and EPS numbers.

Very Strong EPS Growth of 42% Y/Y

Microsoft is clear that it's not resting on its recent performance. In fact, Microsoft continues to signal to investors that it's investing and innovating into its entire tech stack.

What's more, despite the consistent investment, Microsoft's EPS number this quarter was up 42% y/y (non-GAAP, at constant currency).

Furthermore, if we look at Microsoft's trailing twelve-month EPS number of $7.97 we can see that this figure is up 34% y/y (non-GAAP, constant currency).

Given Microsoft's momentum of late, together with Microsoft's CFO Amy Hood's comments on the call that in fiscal 2022 Microsoft would see ''healthy double-digit revenue growth'' we can easily forecast that Microsoft's EPS numbers will climb toat least $10.36 in fiscal 2022.

Valuation - Still Offering a Meaningful Margin of Safety

As noted above, if we are conservative in our assumption for Microsoft's bottom line to grow by 30% y/y in fiscal 2022 this would imply that Microsoft's non-GAAP EPS would reach $10.36.

Note, while this is a deceleration from fiscal 2021 EPS growth of 34%, this would be a step up from the 25% EPS growth in fiscal 2020.

Nevertheless, I believe that 30% CAGR is reasonable given some y/y margin expansion that Hood's mentioned on the call for fiscal 2022.

All together this implies that the stock is priced at 28x forward earnings. Note, this is not a sales multiple, but its EPS figure.

The Bottom Line

For a company growing its bottom line EPS number by 30% CAGR, having to pay 28x its EPS in the current stock market pricing environment strikes me as a bargain opportunity.

Having said that, as I alluded to at the start of the article, given that so many smaller-cap names are now firmly into correction territory, I'm going to continue deploying my capital own into opportunities that I believe over even more compelling valuations. Happy investing.