Summary

- AMD will see limited impact from any attempted price war by Intel in the server sector.

- The biggest problem facing the semi company is keeping up with accelerated demand for computing power.

- Any attempted price war is likely to just cost Intel more margin.

- The stock trades at just 18x '23 EPS estimates favoring in strong server market share gains.

The long worry for Advanced Micro Devices(AMD) shareholders on this rebuild of the business was a price war from the much larger Intel(INTC) to kill their momentum. The current signals of the chip giant engaging in a price war with server chips is odd considering that AMD is supply constrained. My investment thesis remains highly Bullish on the logically cheap stock after this dip back to $100 based on irrational fears of a pricing war and Chinese market contagion.

Server CPU Price War

Over the last week, a lot of the semiconductor news sites have covered the news of Intel engaging in a server chip price war. The chip giant hopes to catch AMD off guard while supplies are limited in order to retain customers.

The problem here is that Intel appears to not understand basic supply and demand. AMD doesn't have extra chips to sell into the market for Intel to warrant price cuts. In essence, Intel will unlikely undercut pricing on chips where AMD can't compete due to a lack of supply. Besides, a major cloud or hyperscale data center company isn't going to choose a server chip supplier based solely on price over the short term. Intel would have to give up margins for an extended period and convince these customers of a product roadmap where the company has failed for years.

At the Deutsche Bank Technology conference last week, AMD CFO Devinder Kumar was clear that supply problems were constantly evolving with substrate issues resolved to the point that the semiconductor company would easily grow the next two years:

We also believe that we can continue this from our overall standpoint with all the work that we're doing from an overall AMD standpoint, both with the customers on the demand side and also supply with our foundry partners, substrate suppliers and ATMP capacity and feel that there is significant room for us to grow out into 2022 and 2023.

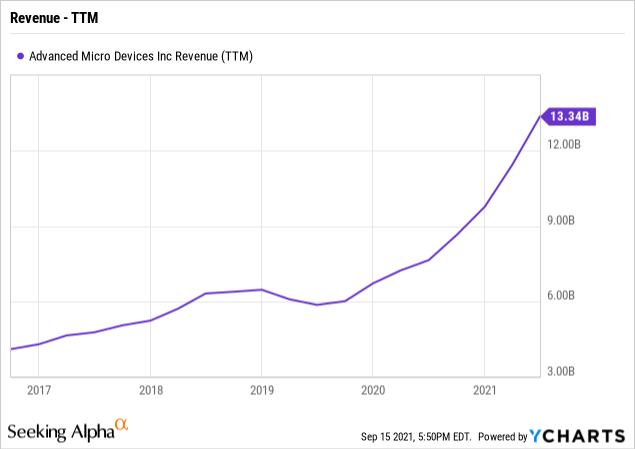

Besides, the supply issues at AMD are as much about accelerating demand for server and gaming chips as much as a lack of the foundries building enough chips. Nobody expected AMD to double revenues from 2019 to 2021.

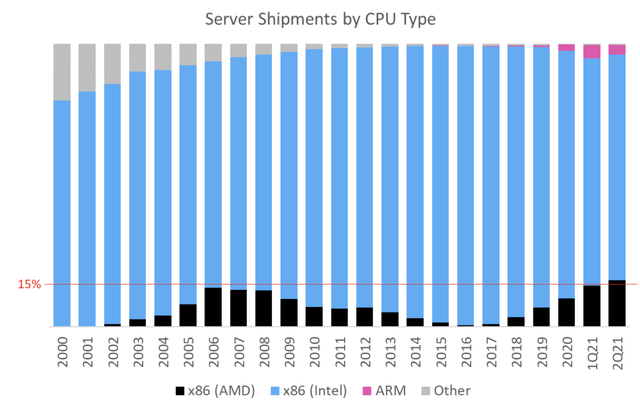

According to research firm Omdia, AMD has already garnered a larger market share position in the server market than back at the prior peak in 2006. In Q2'21 their share of server CPU shipments topped 15% of the market and topped the prior cycle peak back in 2006 at 14%. In addition, the data shows the ARM fears are mostly noise in the sector so far with only 4% of the market. Of course, AMD appears to have the ARM-based chips covered as well.

The data differs from Mercury Research that still has AMD's server market share at just 9.5% in the last quarter, but revenue share jumped to 11.6%. The major difference in the reports is that AMD doesn't compete in all the server markets.

Since the re-emergence of AMD started, questions on a price war by Intel have come up numerous times.DigiTimes reported on apotential price warback in early 2020. On the recent Q2'21 earnings call, CEO Lisa Su made it clear this was already a non-starter:

As you said pricing is not the first order variable when you're buying a server CPU it really is about total cost of ownership. I think the performance leadership that we have, is clearly there, and I think customers see that.

So, we will - we’ll always fight for every socket. I mean that we're very competitive in that fashion. But we think that the way to do that is with the strength of the roadmap and the strength of the deep partnerships, and price is sort of a second order lever in this market.

Intel Giving Up Margin

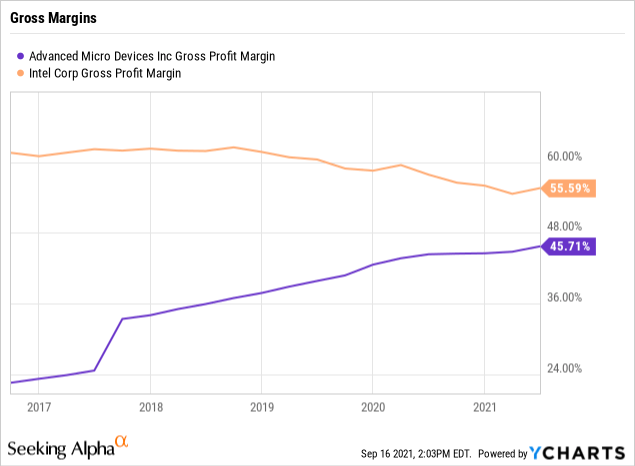

All the price wars over the last few years have done is lead to gross margin deterioration at Intel. AMD continues to grow gross margins despite the pressure placed on margins by semi-customer chips made for the video game consoles. The below numbers are GAAP, but the numbers show that AMD is catching up with the deteriorating margins of Intel. For its part, AMD reports non-GAAP margins of 48% now.

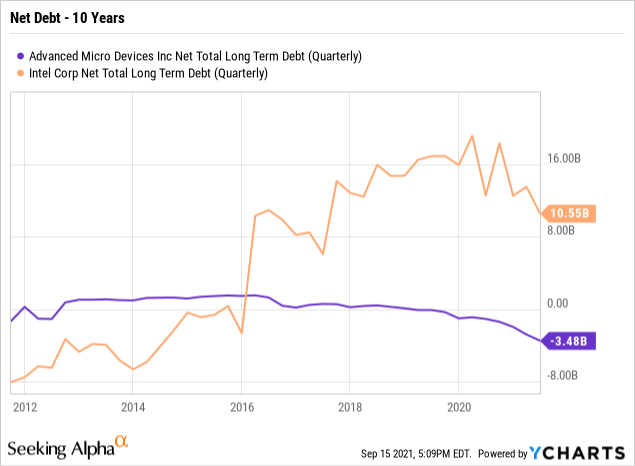

The amazing part is that Intel finds the company in a worse financial position than the company it dominated for decades. AMD now has a net cash position of $3.5 billion while Intel is over $10.6 billion in net debt. Sure Intel generates billions in annual free cash flow, but the company shouldn't have found itself in a position where a price war with AMD is more of an issue for the semi. giant due to their balance sheet.

Takeaway

The key investor takeaway is that AMD appears at no risk from a pricing war by Intel. Neither company has extra chips to compete on price alone unless the company wants to just give up profit for no logical reason.

AMD remains logically cheap based on my prior 2023 EPS estimates of up to $5.50 per share. The stock trades at just 18x such a target and the odds now appear in favor of AMD reaching such a massive target.