Summary

- The latest FOMC meeting confirmed that the imminent rate hikes might be coming sooner than expected.

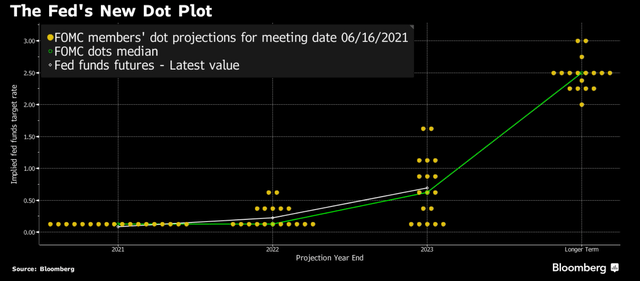

- The quarterly projections showed that the FOMC anticipates two interest rate increases by the end of 2023, inching towards a target rate of 2.5% in the longer term.

- With growth stocks benefiting from the past year of low rates, investors are now left wondering how the upcoming rate hikes will impact Tesla's price performance in the near term.

- We believe the California-based EV maker’s current stock price is already reflective of its upside potential, with the potential impact from upcoming rate hikes already priced in.

Federal Reserve Chair Jerome Powell has confirmed last week that the anticipated timing and pace of interest rate hikes from the current near-zero levels will be pulled forward in response to increasing inflation risks. The quarterly projections showed that the FOMC anticipatestwo interest rate increases by the end of 2023 as opposed to the initially expected timeline of 2024; and the rate hikes will inch towards a target rate of approximately 2.5% in the longer term, akin to the last rate-hike cycle observed between 2015 and 2018.

With growth stocks across the disruptive technology industry, including the electric vehicles (“EV”) sector, benefiting from the past year of low rates, investors have begun to question how the upcoming interest rate increases will impact prospects moving forward. The market has already pulled back from its peak in February following a growth stock sell-off triggered by the jump in government bond yields – notable names within the EV sector, including industry leader Tesla (NASDAQ: TSLA), have been down by more than 20% since. While investors continue to wonder how the upcoming rate hikes will impact Tesla, we believe the California-based EV maker’s current stock price is already reflective of its upside potential and the impact from upcoming rate hikes. The following analysis will showcase how we have arrived at our thesis, and also quantify the potential impact that the upcoming interest rate increases will have on Tesla’s valuation.

The Impact on Tesla’s Effective Interest Rate and WACC

In 2020, Tesla reported annual interest expenses of $748 million, representing approximately 5% of their portfolio of outstanding debt (excluding finance leases). This represents a spread of approximately 350 bps on the current 10-year Treasury yield of approximately 1.5%, which is consistent with the spread to benchmark Treasury of 320 bps on Tesla’s latest issuance of the fixed-rate 2025 Senior Notes.

Based on Tesla’s current debt maturity profile, the company will likely be refinancing a large portion of their debt coming due between 2022 and 2025 in order to support their ongoing capex needs on the construction of new manufacturing plants, as well as R&D spending on technological advancements related to battery cells and autonomous driving. The potential refinancing timeline also coincides with the projected timeline of federal fund rate hikes based on the FOMC’s latest meeting on June 16th.

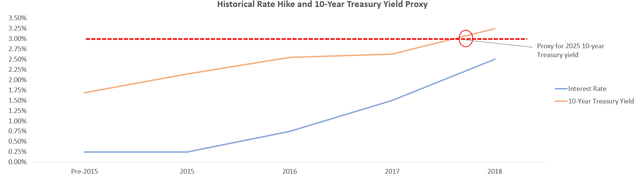

In order to forecast the new cost on Tesla’s future debt refinancing, we have used the historical rate hike trend observed between 2015 and 2018 as a proxy for the timing and extent of upcoming rate increases, and the related historical 10-year Treasury yields as a proxy for projected benchmark Treasury. On this basis, the projected 10-year Treasury yield could exceed 3% by 2025 following the upcoming rate increases.

By adding Tesla’s historical spread of 350 bps to the forecasted benchmark Treasury yield of up to 3% as analyzed above, the effective interest rate that Tesla is expected to pay on their debt profile could rise from the current 5% up to more than 6.5% by 2024 to 2030. Taking this into consideration, we are forecasting interest expense of approximately $534 million by the end of 2021, with growth towards $660 million on an annual basis by the end of the decade, assuming $9.5 billion to $10 billion of outstanding debt based on Tesla’s current capital structure. Based on these projections, the upcoming rate increase’s impact on Tesla’s bottom line will be approximately $126 million of incremental interest expenses on an annual basis from 2026 onwards.

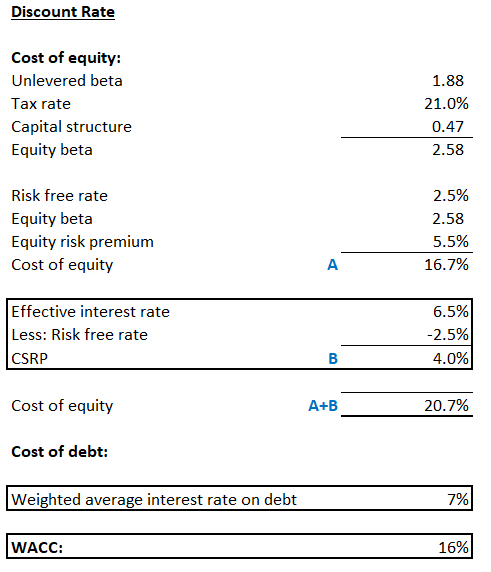

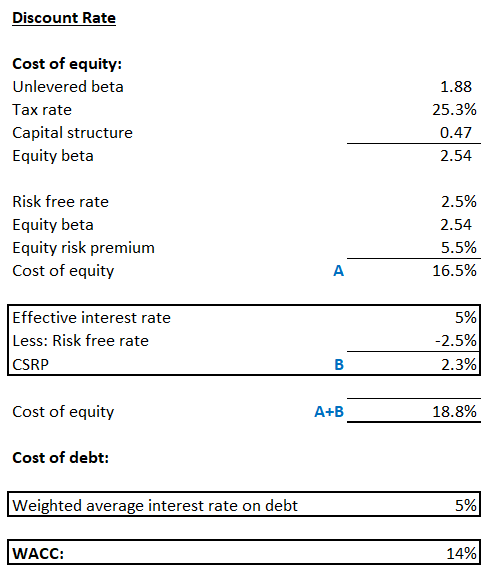

The upcoming rate hikes will also increase the weighted average cost of capital (“WACC”) used to discount the Tesla’s projected free cash flows, which will result in material changes to the company’s valuation. Considering the forecasted increase of Tesla’s effective interest rate on debt to 6.5% on a forward-looking basis and a risk-free rate of 2.5% based on projected 10-year Treasury yield post rate-hikes, Tesla’s company-specific risk premium (“CSRP”) used to compute the WACC would be approximately 4%. The weighted average cost of debt used to compute the WACC would also increase to approximately 7%. This would accordingly result in a WACC of 16% based on Tesla’s current debt-to-equity capital structure:

The Impact on Tesla’s Valuation

In order to evaluate the above-derived WACC’s impact on Tesla’s valuation, we have performed a 10-year discounted cash flow (“DCF”) analysis based on the company’s projected financials. The following will first briefly discuss the growth assumptions used in our projected financials for Tesla over the 10-year discrete period. Then, we will proceed to explain the inputs used in our DCF analysis and compute our valuation for Tesla.

Financial Projections

In our base case forecast, we have applied conservative growth assumptions based on Tesla’s current business environment and growth initiatives, as well as market outlooks obtained from external research.

With government intervention through implementation of strict climate change policies and favourable financial incentives, combined with technological advances made to battery cells and charging infrastructure to extend the travel range of EVs, consumer perception of the new mode of transportation has significantly improved in recent years. Global EV sales are expected to outpace gasoline engines by 2033, which is at least five years earlier than the initial timeline based on narratives from just a few months ago. The industry is projected to grow at a compounded annual growth rate (“CAGR”) of 21.1% into the end of the decade, with China representing the largest market.

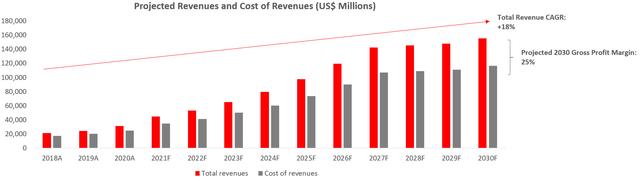

Projected Revenues and Cost of Sales

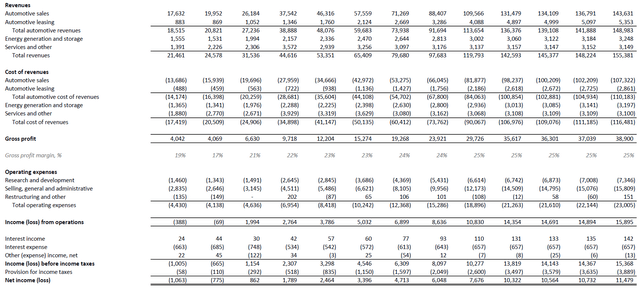

Based on the above growth trends observed across the EV sector, we are projecting revenues generated from the sale and leasing of Tesla vehicles to grow at a CAGR of approximately 20% into FY 2030; this is consistent with the company’s growing presence in the Chinese market, as well as the continuous ramp up in vehicle production and sales observed over the past year and in recent months. We are forecasting automotive revenues to increase by 43% year-over-year to approximately $38.9 billion by the end of 2021, and reach $149 billion by 2030 based on the 20% CAGR. And combined with the anticipated growth of ancillary revenues generated from Tesla’s energy and other services business segments, we are forecasting total revenues of $44.6 billion by the end of the year, and $155 billion by the end of the decade, representing a projected CAGR of 18% into 2030.

Cost of revenues as a percentage of total revenues are expected to improve slightly over time due to cost efficiencies achieved through economies of scale as Tesla’s vehicle and energy generation / storage solutions sales continue to ramp up. We are forecasting total cost of revenues to increase at a CAGR of 17% into 2030, which is in line with our revenue growth projections. This would accordingly result in projected cost of revenues of $34.9 billion by the end of the year and $116.5 billion by 2030, representing gross profit margin improvements from 21% in 2020 to approximately 25% by 2030 which is in line with guidance observed across industry peers such as Lucid Motors (NYSE: CCIV).

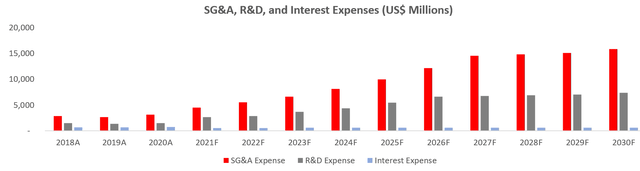

Projected Operating Expenses and Other Expenses

In terms of operating expenses, R&D spending in the foreseeable future are expected to remain consistent with prior years’ at 6% of total revenues to support Tesla’s ongoing advancements in battery cell and self-driving technology development. Meanwhile, selling, general and administrative expenses are projected to maintain at 10% of total revenues moving forward, which is in line with Tesla’s historical cost structure as well as industry trends.

With regards to financing costs, annual interest expenses are expected to fall between $534 million to $660 million from 2021 to 2030. As mentioned in earlier sections, the projections are derived based on the upcoming interest rate hikes, as well as Tesla’s current and projected capital structure.

Projected Earnings

Based on the above considerations, our base case forecast is predicting net income of $1.8 billion by the end of the fiscal year, with expected growth at a CAGR of 20% towards $11.5 billion by 2030.

i. Base Case Financial Forecasts:

Discounted Cash Flow Analysis

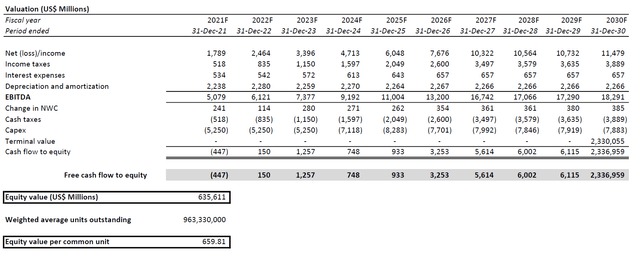

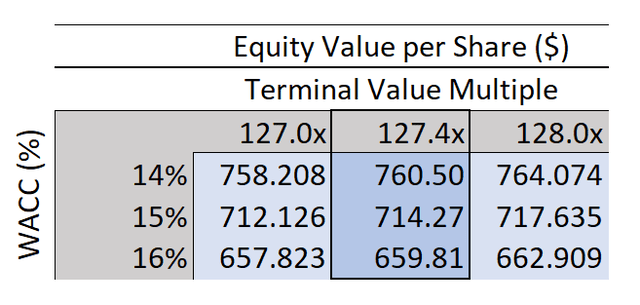

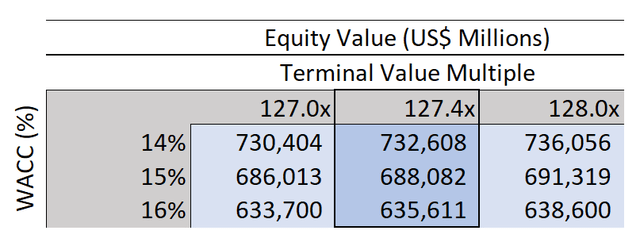

Building on our financial forecasts above, our price target for Tesla is $659.81 based on an estimated equity value of approximately $635.6 billion. Based on our valuation's proximity to Tesla's last traded share price of $688.72 on June 28th, we believe the stock is reasonably priced at the moment.

Our valuation is derived from a 10-year DCF analysis in conjunction with the above forecasted financial information. The base case valuation assumes a 127.4x EV/EBITDA exit multiple, which is consistent with the level at which the stock is currently traded at on a forward-looking basis. We have applied a WACC of 16%, as derived in the beginning of our analysis based on Tesla’s current risk profile, capital structure, and impacts from upcoming rate increases, to arrive at our projected price target.

Quantifying the Impact of Rate Hikes on Tesla’s Valuation

In order to quantify the potential impact of upcoming interest rate increases on Tesla’s valuation, we have also performed a sensitivity analysis using a WACC of 14% derived based on the company’s current effective interest rate of 5%.

Holding the forecasted cash flow streams and exit multiple used in our DCF analysis above constant, a WACC of 14% would yield an equity value of approximately $732.6 billion, or $760.50 per share. This drives a difference in value of $97.0 billion, or $100.69 per share, compared to our valuation using a WACC of 16%. The difference accordingly represents the potential quantified impact that the upcoming rate hikes will have on Tesla’s intrinsic value.

Conclusion

Based on the foregoing analysis, we believe Tesla’s current share price is reasonably reflective of the company’s upside potential, with the upcoming interest rate increase impacts to their intrinsic value already priced in. As such, we are assigning a Neutral Rating on the stock at this time.

However, as discussed in our analysis of Tesla's financial projections, the company's ongoing developments to their proprietary battery cell and self-driving technology make them a leading contestant in the global EV arms race. And Tesla's future commercialized deployment of said technologies will be critical catalysts for price appreciations that could compensate beyond the impact from upcoming rate hikes in the long-run. The fast-approaching release of second quarter results and delivery updates will also be a tell-tale of where Tesla currently stands, and a near-term catalyst to look out for.