1Q22 ER

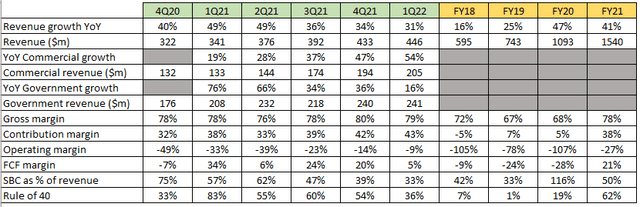

Figure 1 - Key Financials Overview

Convequity

Bearish points

- 1Q22 government business growth decelerates to 16% YoY, particularly surprising given the Russia-Ukraine War and rising geopolitical tensions. This drop in government growth appears to have recoiled the stock from the previous bullishness priced in during the initial succeeding weeks following Russia’s invasion. Management has explained that government growth will reaccelerate, however.

- 2Q22 revenue YoY growth guidance declines to 20% >>> though management explained they expect a reacceleration in 2H22.

- The Rule of 40 – growth plus FCF margin – has declined sharply to 36% in 1Q22. It seems as though the double whammy of overall growth only being a whisker higher than the long-term guidance of 30%+ combined with a steepish drop in FCF margin has put off investors. Investors should bear in mind, however, that FCF margin is volatile for software stocks, especially for firms like PLTR involved in lengthy procurement timelines and very large deals.

Bullish points

- Government business growth is expected to reaccelerate in 2H22.

- 40 net new customer adds in 1Q22 – this is compared to c. 100 in FY21 and only six in FY20. At this rate of customer growth, there will be 160 net new customers in FY22. This is what has really caught our attention. PLTR is finding operating leverage and scaling out its business with lower friction for customer onboarding. And it’s possible that if PLTR has accelerated customer onboarding this quick, then perhaps S&M resources have been spread too thin to drive the land-and-expand sales, thus depressing the overall growth somewhat.

- Commercial growth has now accelerated for five sequential quarters – rising to 54% YoY growth in 1Q22.

- The contribution margin gradually improved in 1Q22 despite the influx of new customers. Just imagine when PLTR has 1000s of customers and the new customers each quarter represent a much smaller percentage of the total customer base... this means PLTR’s overall contribution margin is going to be way closer to the Scale Phase contribution margin of c. 75% (it’s actually close to 90% for very large Scale Phase customers).

- 1Q22 operating margin was -9%, showing steady progress toward breakeven.

- SBC as a percentage of revenue is declining at a solid pace. We expect it will normalize toward 10%-20% - which appears to be a typical range for multibillion dollar revenue software firms – within the next couple of years.

Once PLTR has further optimized its S&M operations (remember that they only began in 2020), the large influx of new customers combined with the presumably low initial land/expand momentum, presents substantial durable growth for the coming quarters.

Long-Term Profitability Potential

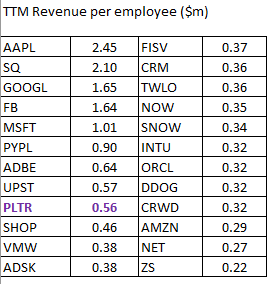

For the bears who believe PLTR won’t be a highly profitable company, they should consider the following table. PLTR is generating revenue per employee of $560k, which is almost midway between the average (that is, our estimate of the average based on doing quite a few of these calculations) of $250k-$350k to the beginning of tech giant range – or even further than midway if you use ADBE as the start of the tech giants’ range. We like this metric because it gives a glimpse into the core unit economics and is very insightful for assessing future profitability of GAAP loss making firms.

Figure 2 - Revenue Per Employee

Convequity

All the firms with high revenue per employee are complete dominators in their core market – hence why they’ve become tech giants – and they are highly profitable (except for SQ at present). PLTR is generating $560k per employee with only c. 280 customers to date. So, investors should expect this metric to move deep into the tech giant range when PLTR scales into 1000s of customers – we’ll touch on this likelihood later – which should translate into high profit margins.

Our Overarching Thesis

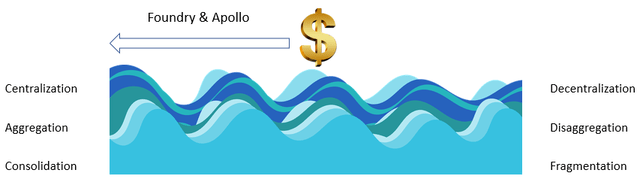

Our overarching thesis is predicated on the observation that technological evolution is merely a back and forth between centralization/aggregation/consolidation and decentralization/disaggregation/fragmentation. Time and time again we’ve seen one-of-a-kind companies appear with the objective of dominating and radically changing the landscape via the former and then niche players will emerge aiming to deliver specialized services via the latter.

We’ve seen this with IBM in the 1960s with mainframes, Intel with the microprocessor in the 1970s, Microsoft with Windows in the 1980s, Apple in the 2000s with iOS, and also Amazon in the 2010s with AWS. We anticipate we’ll see this happen for PLTR in the 2020s with Foundry and Apollo. In essence, PLTR will provide a consolidated way of managing data, building applications, and deploying those applications in an increasingly decentralized technological environment.

Figure 3 - Technological Evolution is Merely Waves Swinging from One Side to the Other

Convequity

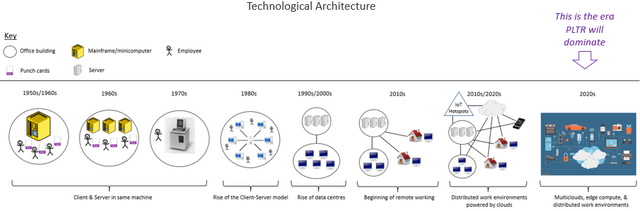

The following diagram depicts the market need for something like Foundry and Apollo, whether or not organizations realize this at present.

Figure 4 - PLTR Can Provide Consolidation in an Increasingly Fragmented Technological World

Convequity

Just like Windows provided consolidation by providing a single compatible OS for the highly fragmented PC market in the 1980s/90s, PLTR can provide consolidation by providing a single compatible OS for the fragmenting cloud and edge compute architectures. In essence, PLTR will do this via three channels: data (Foundry), AI/ML (Foundry), and software deployment (Apollo).

Core Channels of Growth

There are many ways in which to slice and dice what PLTR does, though at a high-level our take is that PLTR’s sustainable advantages relate to data, AI/ML, and software delivery/deployment.

Data, AI/ML, and software delivery are colossal markets that are foundational to the progress of so many other huge potential markets - and PLTR is the absolute leader in each of these areas. We’re passionate about cybersecurity, but even this huge growthy market is being driven via better data management and AI/ML. Edge compute is another huge potential market but will only progress toward its potential if innovations in data management, AI/ML, and software delivery continue.

Data

This is an extremely broad area but PLTR excels in all of it thanks to its SDDI (Software-Defined Data Integration). From data source connections, to transforming data to useful datasets, to creating ontologies so that users can clearly understand the relationships of every piece of data ... which then enables a robust data fabric in which to generate company-wide business insights and build highly effective applications. Fundamentally managing data more effectively is the core driver for any market and inefficient ways of handling data is the number one headwind to faster digitalization. PLTR is the only vendor capable of breaking down the data siloes and offering an end-to-end data processing and analytics platform.

AI/ML

The AI/ML value/supply chain has parts which have become commoditized and other parts in which there is still lots of opportunity for vendors to differentiate and solve complex problems. There are many ways to describe the AI/ML value chain, though we’ll go with this:

Data source connections feature engineering, data labelling, data transforming, or ETL/ML model training, ML model validating, making the ML model interoperate with other systems and then staging and then production.

Parts like feature engineering, data labelling, and ML model training, for some areas of AI/ML (i.e., computer vision), have become commoditized and others will likely become so soon. The others are problem areas for AI/ML to become widely used, and presumably are some of the areas that cause 87% of AI/ML projects to fail.

The parts of the AI/ML we’ve highlighted in bold are the MLOps components. This is a huge area of innovation because it is an extremely complicated stage of the value chain. For organizations that can get good data, then take off-the-shelf solutions for feature sets, data labelling, and model training, then integrate an accurate model into an application or make it a service for a pre-existing application, and then have it interact with a single user, is usually doable for the majority of organizations. However, the problems arise when the ML model then needs to interoperate with all the other systems and then have the supporting infrastructure scaled to operationalize it during the staging and then the production stage – this is where MLOps can ease the pain.

All of PLTR’s skills rooted in data, AI/ML, and software deployments, have enabled them to offer a seamless market-leading MLOps solution. And within the AI/ML supply chain, we think that MLOps is probably the number one determinant for AI/ML project success at present.

Another key competitive advantage for PLTR in the AI/ML space is their edge AI solutions. Deploying AI at the edge requires algorithms that can operate in low power and low bandwidth environments, and thanks to PLTR’s long enduring experience in data management and training AI/ML models, they now have an unparalleled advantage. Such models need to operate on highly filtered data streams and as PLTR’s core expertise is sorting through data, it’s no surprise that they are leading in this edge AI space.

Software Delivery/Deployment

Software delivery/deployment is a colossal area of innovation. Developers now have to build their applications and then work through deploying it in various different hosting environments – multiple different clouds, on-prem, in edge spaces, in different compliance jurisdictions. And each host will have particular things that developers need to do in order to make their software work properly.

PLTR has Apollo Cloud for this pervasive problem. Apollo was initially just used internally to deliver an average of 41,000 updates per week for Gotham and Foundry – last year it was expanded to Apollo Cloud which can deliver any non-PLTR software to any hosting environment. Apollo is what has enabled PLTR to release updates and new features with such rapidity, because developers just write the code and then push the deployment aspects to Apollo. The same technology is alleviating the various deployment pain points for developers and organizations all over the globe.

We compare this directly to what Amazon did with AWS – offer out an internally used resource to third party clients. It has the potential to give PLTR a much larger and richer feedback pool in which to improve their own software delivery processes whilst also generating a huge additional revenue stream.

However, according to CodeStrap on YouTube (we definitely recommend readers watch his content), there is execution risk emerging with Apollo Cloud. There are smaller players offering solutions to developers whereby they can just push their application to them and they’ll provision the IaaS and deploy their applications. And VMware also has a solution similar to Apollo Cloud. At present, PLTR has the clear advantage thanks to everything else it offers and the sheer autonomy of Apollo, though this will not be sufficient to stop the market going to alternatives. As CodeStrap explains, PLTR needs to make the entry barriers for Apollo Cloud and Foundry lower in order to lower onboarding friction and speed up the customer count.

Can PLTR Get The Flywheel Effect In Motion?

Up until very recently, PLTR has been closed off to the outside developer community. There is substantial vetting going on to ensure Foundry applicants are suitable to get the most out of the OS and also that they align with PLTR’s core values. Although, in the last couple of weeks PLTR has launched a site dedicated to helping developers learn how to use Foundry with loads of documentation, which is a significant milestone toward eventually allowing anybody to pay for Foundry with a credit card and get started super quickly. This could mitigate the execution risk outlined in the previous section, but investors would definitely like to see further progress to make it easier to get started with Foundry.

Gaining adoption throughout the developer communities is the key to generating the flywheel network effect that ourselves and other analysts have discussed previously. And no doubt this is a solid step in the right direction to make this happen.

Valuation

We remain very bullish over the long-term because relatively and in absolute terms, PLTR is grossly undervalued. Amid the heightened geopolitical risk, we are now seeing the highest possibility of a nuclear attack in our lifetime since the Cold War. Various European countries, Germany especially, are ramping up military and defense spending. Furthermore, supply chain crises, inflation concerns, and ongoing digital disruption, are all posing a huge risk for organizations as they are inherently slow to change, all of which offers PLTR a very large and durable growth runway. Thus, we believe the 30%+ growth guidance through FY25 by management is likely and our DCF valuation values the stock within a range of $25 to $35 per share.

PLTR’s forward EV/GP also illuminates the attractiveness of the stock right now. Based on an EV of $14,810m, TTM gross profit of $1,287m, and a NTM growth of 30%, we arrive at an EV/GP/Growth of 0.38, which is very low for a high-growth BoB software firm. PLTR’s NTM EV/S of c. 7x also shows that the stock is trading close to half that of legacy tech names. Multiples based on items further down the income statement are indeed less attractive, though for us and many other high-growth software investors, given PLTR’s growth outlook and immature operations, we will focus more on these multiples when growth further matures. Additionally, the high gross margin, revenue per employee, and other business metrics, give us comfort that PLTR will eventually be very profitable.

Conclusion

Along with the general macro gloom, short-termism has dragged down the stock but in the long-term the risk-reward is highly attractive. There are execution risks because PLTR has long had superior software though has only accumulated c. 280 customers to date. Developers, data scientists, and data engineers, won’t wait around much longer before opting for alternatives to solve their most complicated problems - hence PLTR needs to lower the onboarding frictions ASAP. Although, recently we’ve seen signs of PLTR offering easier onboarding (i.e., the developer site) so that is really positive.

If PLTR can execute, then durable growth will prevail and the firm will maximize its highly profitable unit economics. We believe if PLTR can execute then in five and 10 years, we’ll look back at this point in time and define this as the beginning of the next era of technological evolution whereby PLTR provided much needed consolidation for an increasingly complex, fragmented and decentralized technological landscape.