Bearish Crude Reports Trigger a Sharp Selloff: How to Use Options to Trade a Choppy Market?

Ahead of OPEC’s monthly market analysis and the IEA’s annual energy outlook this week, WTI steadied after three straight up days, signaling a shift from chasing strength to waiting on new data. Traders are focused on Wednesday night’s OPEC release and the forthcoming IEA outlook.

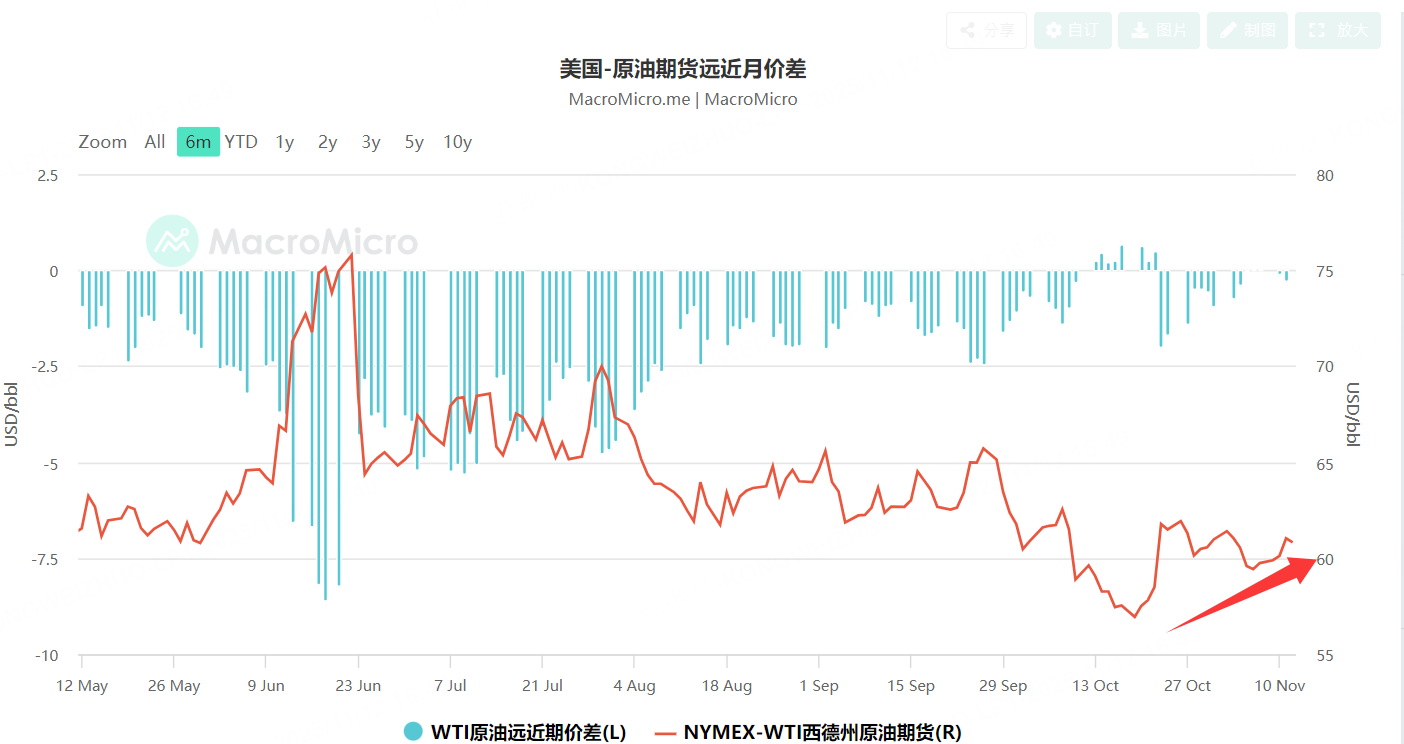

Curve signals

The WTI term structure has seen the spread between far-month and near-month contracts narrow markedly, a classic sign that inventories are moving from tight toward looser in the physical market. Since the October 20 bottom in WTI, far-month vs near-month spread have kept compressing, implying faltering buy interest in near-month and a supply backdrop shifting from tight to more ample. Throughout the year, worries about a “large surplus” in crude have dominated price action and underpinned persistent weakness, pushing WTI steadily lower with descending bottoms

Supply, inventories, constraints

OPEC and allies including Russia have been restoring capacity this year, while non-OPEC producers are also ramping up, making broad-based supply expansion a market consensus. The IEA projects crude supply to hit a record next year, and houses like Goldman Sachs warn inventories will keep rising, jointly forming a hard cap on upside.

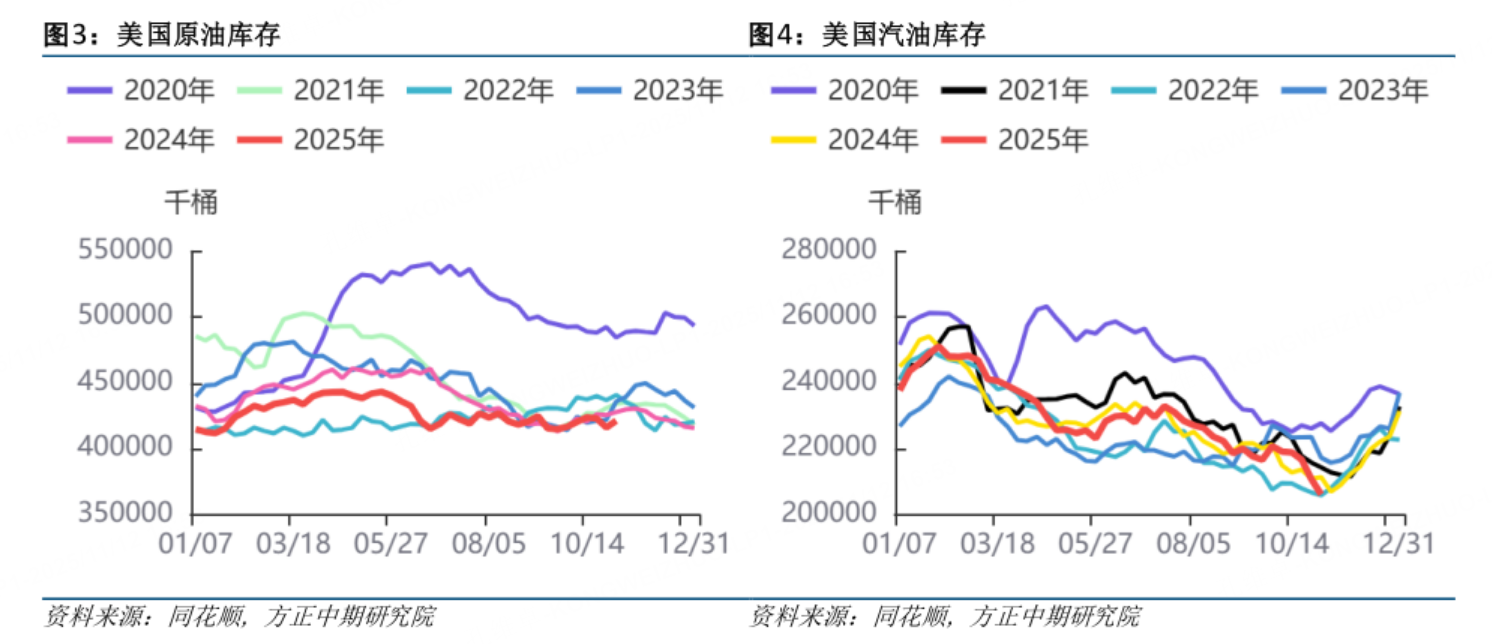

U.S. crude and gasoline inventories haven’t swung dramatically this year, but levels sit near the lower bound of the five-year average range; even so, seasonal patterns point higher ahead, and combined with increased output among producers, upside in crude appears constrained.

But,on the other hand, at the same time Supportive factors still matter.!

Europe is seeking to separate Lukoil from national energy systems, keeping the prospect of near-term fuel price increases alive and raising the risk of intermittent tightness along refined products chains. Sanctions on Lukoil PJSC and Rosneft PJSC aimed at pressuring Russia over the Ukraine war have directly lifted diesel prices。

In response, two Indian refiners recently bought a combined 5 million barrels on the spot market from the U.S., Iraq, and the UAE to partially replace Russian supply, signaling resilient demand. These purchases stem from last month’s sanctions on Rosneft and Lukoil, which together account for roughly half of Russia’s oil exports and a meaningful share of India’s imports.

Market state: capped upside, supported downside

Crude likely sits in a state where upside is limited but downside is cushioned.

Upside is capped by simultaneous supply restoration and expansion across OPEC+ and non‑OPEC, shifting the marginal supply curve right and suppressing price elasticity to the upside, and by IEA’s record-supply forecast plus inventory-build warnings anchoring expectations and dampening trend-long risk premia.

Downside is supported by sanctions-induced diesel price strength and policy actions to preserve operations, tightening refined products temporarily, and by Europe’s Lukoil separation push that keeps the near-term prospect of higher fuel prices on the table.

Strategy: sell puts below prior lows

A rolling program of selling WTI puts below prior lows can monetize this backdrop. For those without futures options access, consider low-strike puts on USO or XLE as proxies.

Example: XLE put

Using a put on XLE expiring in nine days with a strike at 86, the theoretical breakeven is around 83.3 at expiry; if price holds above that in nine days, selling one put would collect about $257.5 in premium.

Nov 13 update

The latest EIA report lifted the 2025 U.S. production forecast from 13.51 mbpd to 13.58 mbpd, and OPEC said global supply exceeded demand in Q3, intensifying surplus concerns and suggesting the long-anticipated glut has materialized.

After Wednesday’s plunge, crude extended losses: WTI fell to $58/bbl, the biggest drop since June, and Brent slipped below $63/bbl.

Given the update, shift from the standalone short-put to a combined stance: be short XLE while maintaining the sell-put overlay to hedge the risk of a WTI rebound near prior lows; this remains a conservative approach under heightened one-way downside pressure in the near term.

$NQ100指数主连 2512(NQmain)$ $SP500指数主连 2512(ESmain)$ $SPDR能源指数ETF(XLE)$ $道琼斯指数主连 2512(YMmain)$ $天然气主连 2512(NGmain)$

Disclaimer: Investing carries risk. This is not financial advice. The above content should not be regarded as an offer, recommendation, or solicitation on acquiring or disposing of any financial products, any associated discussions, comments, or posts by author or other users should not be considered as such either. It is solely for general information purpose only, which does not consider your own investment objectives, financial situations or needs. TTM assumes no responsibility or warranty for the accuracy and completeness of the information, investors should do their own research and may seek professional advice before investing.

- Phyllis Strachey·2025-11-13$58 WTI + surplus confirmation = deeper downside before a bounce!LikeReport

- JackPowell·2025-11-13Short XLE puts still look juicy here. Staying nimble until OPEC speaks 🧐LikeReport

- Wade Shaw·2025-11-13How low can WTI go with EIA’s 2025 production hike?LikeReport

- Ron Anne·2025-11-13XLE short + put sell balances near-term risk perfectly now!LikeReport